Your mortgage is likely one of the largest financial commitments you’ll ever make. Yet, many homeowners set it and forget it, missing out on potential benefits. Just like you wouldn’t ignore your health or car maintenance, it’s crucial to take a close look at your mortgage regularly. A periodic review can uncover hidden savings and significantly impact your financial well-being.

With interest rates fluctuating and new loan products hitting the market constantly, there’s an opportunity waiting for those willing to dive deeper into their mortgage situation. Let’s explore why reviewing your mortgage should be part of your regular financial check-up routine and how those reviews could lead to substantial savings in the long run.

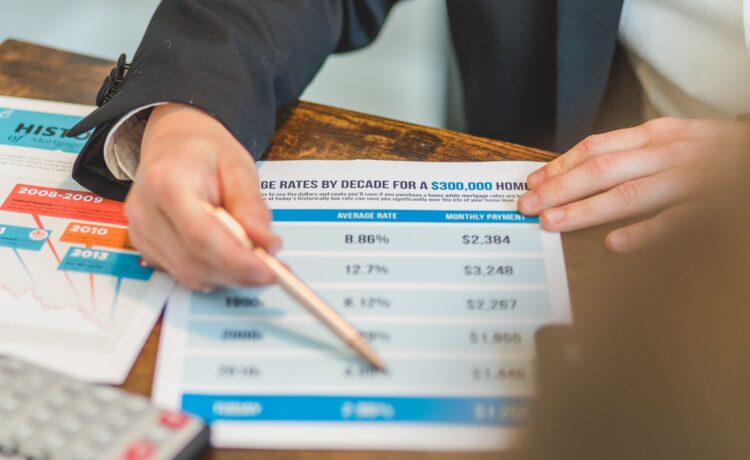

The potential savings from reviewing your mortgage

learn more about refinancing your mortgage which can lead to significant savings. Many homeowners overlook this simple yet effective strategy.

Interest rates fluctuate frequently, and what was once a competitive rate may no longer be the best deal available. By comparing current offerings, you might find lower rates that could drastically reduce your monthly payments.

Additionally, fees associated with loans change over time as well. Lenders often introduce promotions or reduced closing costs that could benefit you.

You might also discover opportunities for loan adjustments that fit your financial situation better—like switching from an adjustable-rate mortgage to a fixed-rate option for stability.

Each percentage point saved on interest can add up significantly over the life of the loan, making regular reviews essential in maximizing your financial health. The potential gains are more than just numbers; they represent real cash in your pocket each month.

How often should you review your mortgage?

It’s a common question: how often should you take a look at your mortgage? While each situation is unique, an annual review can be beneficial.

Life changes quickly, and so do interest rates. An annual check-in allows you to stay informed about market trends that could impact your payments.

Additionally, consider reviewing your mortgage after any significant life events—like a promotion or the birth of a child. These moments might change your financial landscape, making it wise to reassess.

If you’ve made improvements on your home or if property values in your area have risen significantly, these factors also warrant a closer look at your current mortgage terms.

Staying proactive ensures you’re not leaving potential savings on the table. Regular reviews keep you aligned with both personal goals and market conditions.

What to look for when reviewing your mortgage

When reviewing your mortgage, start by examining the interest rate. Is it competitive compared to current market rates? A small reduction can lead to significant savings over time.

Next, look at the terms of your loan. Are you on a 30-year fixed rate or something shorter? Adjusting the term could impact monthly payments and long-term costs.

Consider any fees associated with your mortgage. Origination fees, closing costs, and prepayment penalties can add up quickly. Understanding these will help you make informed decisions.

Don’t forget about your equity position. If property values have risen in your area, you may have more equity than before. This could open doors for refinancing options or better rates.

Evaluate customer service from your lender. Responsive support can make all the difference during the life of a mortgage. Look for reviews and testimonials from other borrowers to gauge their experiences.

The benefits of refinancing your mortgage

Refinancing your mortgage can unlock a range of financial benefits. It allows homeowners to adjust their loan terms, potentially leading to lower monthly payments and reduced interest costs over time. For many, refinancing translates into significant savings — sometimes hundreds of dollars each month.

Additionally, if property values in your area have increased, refinancing might enable you to tap into your home’s equity. This can provide funds for home improvements or other investments that could further enhance your financial position.

Another key advantage is the opportunity to switch from an adjustable-rate mortgage (ARM) to a fixed-rate mortgage. Fixed rates offer stability against market fluctuations and are beneficial in environments where interest rates are on the rise.

Refinancing can consolidate debt by allowing you to borrow more than what you owe on your current mortgage. This strategy could simplify finances by combining various debts into one manageable payment with a potentially lower interest rate overall.

Regularly reviewing and possibly refining your mortgage isn’t just about saving money; it’s also about ensuring that your financing aligns with changes in life circumstances and economic conditions. Taking proactive steps today could shape a brighter financial future tomorrow.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}